Sole Trader vs Company in Australia: Which Pays Less Tax?

If you're starting or running a business in Australia, choosing the right structure is one of the most important financial decisions you will make.

The two most common options are operating as a sole trader or setting up a company (Pty Ltd). At first glance, many people assume that a company will always result in lower tax. In practice, the answer is more nuanced.

The right choice depends on your income level, how you plan to use your profits, and your long term goals.

What is a Sole Trader

A sole trader is the simplest business structure in Australia. You operate the business in your own name or under a registered business name, and there is no legal separation between you and the business.

All income earned by the business is treated as your personal income, and you are personally responsible for any liabilities.

This structure is easy to set up, has low ongoing costs, and is commonly used by freelancers, contractors and small operators.

How Sole Traders Are Taxed

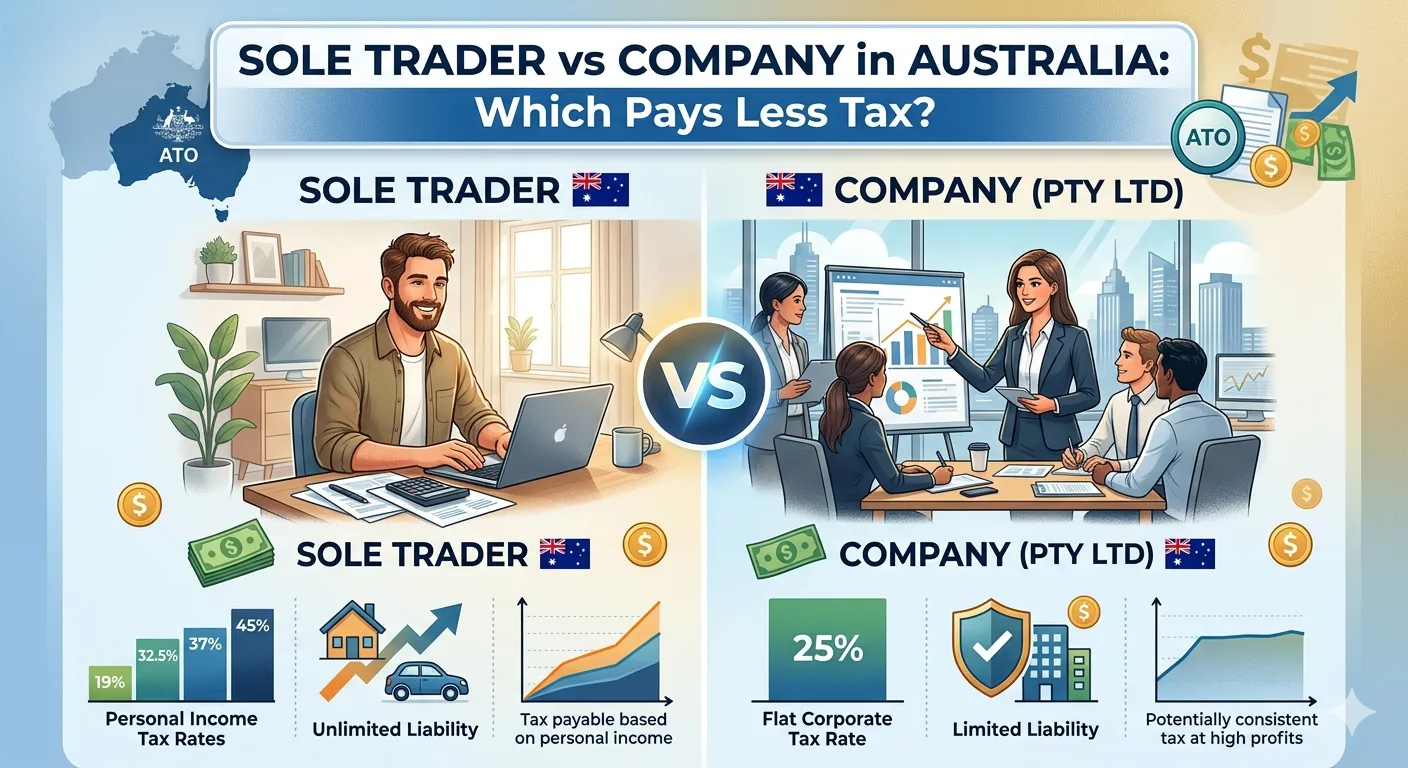

As a sole trader, your profit is added directly to your personal income and taxed using individual tax rates.

Australia uses a progressive tax system. This means that as your income increases, higher portions of your income are taxed at higher rates.

For example, if your business generates a profit of $100,000, that amount is included in your personal tax return and taxed accordingly.

This approach is straightforward, but it becomes less efficient as income increases, because higher marginal tax rates apply.

What is a Company

A company is a separate legal entity from its owners. This means the business operates independently, and liability is generally limited to the company itself.

Companies in Australia are typically set up as proprietary limited (Pty Ltd) entities and require registration with ASIC.

While this structure involves more compliance and administrative requirements, it offers greater flexibility and potential tax planning opportunities.

How Companies Are Taxed

Companies are taxed at a flat rate. For most small businesses, this rate is currently 25%.

At first glance, this may seem lower than individual tax rates. However, this is only part of the picture.

When profits are distributed to shareholders as dividends, those amounts are included in the individual's personal income. Depending on their total income, additional tax may apply.

Franking credits are used to prevent double taxation, but they do not eliminate tax altogether. They simply adjust the final outcome.

As a result, the combined tax paid at the company and personal level can be similar to what would have been paid as a sole trader.

Real World Comparison

Consider a business generating $120,000 in profit.

As a sole trader, the full $120,000 is taxed at individual rates. After tax, the remaining income depends on applicable tax brackets and deductions.

As a company, the business pays 25% tax, leaving $90,000 after tax. If this amount is distributed to the owner, additional tax may apply depending on their personal situation.

In many cases, the final difference between the two structures is smaller than expected, especially at moderate income levels.

This is where many business owners are surprised. The perceived tax advantage of a company does not always materialise in practice.

When a Sole Trader Structure Makes Sense

A sole trader structure is often appropriate in the early stages of a business.

It tends to work well when income is relatively low or moderate, and when most of the profits are withdrawn for personal use.

It is also ideal for those who want minimal administrative burden and lower accounting costs.

For many individuals earning under a certain threshold, the simplicity of this structure outweighs any potential tax benefits of a company.

When a Company May Be More Effective

A company structure becomes more relevant as income increases or when profits are not fully withdrawn.

If you plan to retain profits within the business for reinvestment, the company tax rate can provide a timing advantage.

Companies also allow for more flexibility in structuring income, including paying salaries, distributing dividends, and potentially involving other shareholders.

In addition, a company provides a level of asset protection that does not exist for sole traders.

Key Factors That Influence the Decision

The choice between sole trader and company should not be based on tax alone.

Several factors need to be considered, including:

- Your expected income now and in the future

- Whether you plan to reinvest or withdraw profits

- Your exposure to business risk

- The level of administrative complexity you are willing to manage

- Whether you have international income or assets

Each of these elements can significantly change the outcome.

Common Mistakes

One of the most common mistakes is setting up a company purely to reduce tax, without understanding how distributions are taxed.

Another is delaying the transition to a company when the business has already grown beyond the point where a sole trader structure is efficient.

Some business owners also fail to consider long term strategy, focusing only on short term savings.

In practice, restructuring later can be more costly than making the right decision from the beginning.

Final Thoughts

There is no single structure that is always better.

At lower income levels, the difference in tax is often minimal. As income grows or business complexity increases, a company may offer advantages.

The key is understanding how each structure works in your specific situation.

Making the wrong choice can result in unnecessary tax, higher costs, and additional complexity down the track.

Need help choosing the right structure

If your situation involves higher income, multiple revenue streams, or international elements, the decision becomes less straightforward.

A tailored assessment can help identify the most efficient structure based on your current position and future plans.